6855744

Description

Flashcards by Soon Maple, updated more than 1 year ago

|

|

Created by Soon Maple

about 8 years ago

|

|

| Question | Answer |

| Time Series Decomposition Model | yt = pattern + error yt = (Tt+St+Ct+It) where Tt is the trend component, St is the seasonal component, Ct is the cyclical component and It is the irregular or error component. |

| Time series patterns: Trend | The systematic, long term increase or decrease in a a time series. |

| Time series patterns: Seasonal | A systematic change in the mean of the time series due to seasonal factors. Seasonality is always of a fixed and known period. |

| Time series patterns: cyclic | Fluctuations in the time series that are not part of a fixed period. |

| Additive or Multiplicative? | 1. The additive model is useful when the seasonal variation is relatively constant over time. 2. The multiplicative model is useful when the seasonal variation increases over time. |

| Smoothing | Smoothing means to use all available data to average out irregular or other components from a time series. |

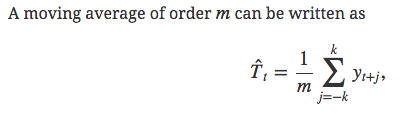

| Moving Average Smoothing | The estimate of the trend-cycle at time t is obtained by averaging values of the time series within k periods of t. m = 2k + 1. |

| What does Moving Average Smoothing do to the time series and how? | MA is a smoothing method and thus captures the main movement of the time series without all the minor fluctuations. MA averages observations that are nearby in time, and thus those observations that are also likely to be close in value. This eliminates some of the randomness in the data, leaving a smooth trend-cycle component. |

| Explain m-MA and the implications of the value m? | An m-MA means a moving average of order m (m = 2k+1). A moving average of order 5 refers to a 5-MA and is the average of the observations in the five year period surrounding either side of the corresponding year. The order of the moving average determines the smoothness of the trend-cycle estimate. In general, a larger order means a smoother curve. Simple MA usually is of odd order. This is so they are symmetric: in a moving average of order m=2k+1 there are k earlier observations, k later observations and the middle observation that are averaged. But if m was even, it would no longer be symmetric. |

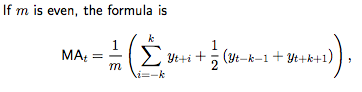

| What are the MA options? | 1)If m is even, the average would no longer be symmetric. m=2k+2 2)We can also conduct a moving average of a moving average. One reason for doing this is to make an even-order moving average symmetric. The notation “2×4-MA” means a 4-MA followed by a 2-MA. It is now a weighted average of observations, but it is symmetric. 3) Weighted MA: Combinations of moving averages result in weighted moving averages. For example, the 2x4-MA discussed above is equivalent to a weighted 5-MA. |

| What and how does a moving average do to a seasonal pattern in a time series? | When there is a seasonal pattern with seasonal period m, applying a moving average of order m (or any multiple) smooths out the seasonality. For example, with monthly data, a MA-12 or a 2-12MA The seasonal variation will be averaged out and the resulting values of T̂ t will have little or no seasonal variation remaining. |

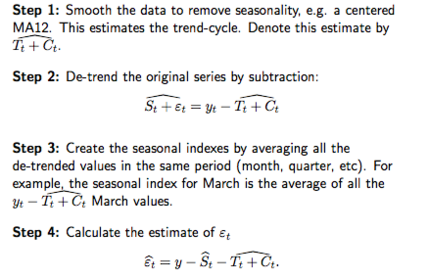

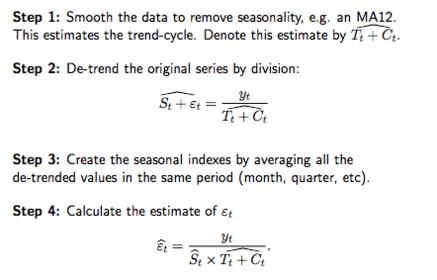

| What is the Classical Decomposition procedure and its assumptions? | * It is a relatively simple procedure and forms the basis for most other methods of time series decomposition. *There are two forms of classical decomposition: an additive decomposition and a multiplicative decomposition *We assume that the seasonal component is constant from year to year. These m values are called the “seasonal indices”. |

| Outline the additive decomposition procedure. | |

| Outline the multiplicative decomposition procedure. | |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.