Description

|

|

Created by hope coull

about 11 years ago

|

|

Page 1

Assets and Liabilities A balance sheet is simply a statement of what the company owns (its assets) and what the company owes out (its liabilities). As we will see, the amount of assets will always be the same as the amount of liabilities. Imagine a set of scales; if we write assets on one side and liabilities on the other, because they both add up to the same amount, the scales will ‘balance’. Capital-Wealth in the form of money or property, used or accumulated in a business by a person, partnership, or corporation.

Creditor-Someone/a company you pay money back at a later date also known as a payable.

Debtor-Someone who owes you money-Receivable

Points to Note 1. It is important to keep the figures in neat columns – directly under the £ signs. 2. Individual figures are put under the first £ sign (for both assets and liabilities). One line is drawn under the list and the total is put, one line down, under the second £ sign. 3. The totals under the second £ sign are then added. Two lines are drawn under the final figures. 4. The balance sheet should still balance!

Liabilities We can split up the liabilities in the same way as we split up the assets. There are two types of liabilities: Current Liabilities – this is what we owe now but will not owe in 12 months. Examples are creditors (who will want their money in the next month or so) and a bank overdraft or loan. Long-Term Liabilities – this is what we owe now and will still owe in 12 months and probably for longer. Examples are capital (as the owner invested the money for many years) and a mortgage (long-term loan on premises).

Assets We have seen that ‘assets’ are what the business owns. These can be split up according to how long we intend to keep them. There are two types of assets: Current Assets – this is what we own now but will not own in 12 months as they constantly change. Examples are stock, debtors, bank and cash. Yes, we will have stock in 12 months but it won’t be the same stock. We will also have cash in 12 months but it won’t be the same notes and coins. Fixed Assets – this is what we own now and will still have next year and probably for longer. Examples are premises, equipment, fixtures and fittings (furniture), and a van.

Budget: Forward finantual planBudgetry control: Moniter the figures of your budget.

Cash flow: Money coming in or out of the buissnessCash flow forecast: To predict how much you haveWhy make a flash flow forecast? To solve problems you might have.

For a minus figure, USE BRACKETS

Increace revenueGet a cheaper supplier or arange a deal with your current supplier.Advertising will increace sales but will cost money.Increace prices but people might not buy. Reduce price people might buy them

Statement of finantual position or balence sheet tells you assets and liabilities

Working captal is the amount of money that i have to run said buisness.Current assets-current liabilities

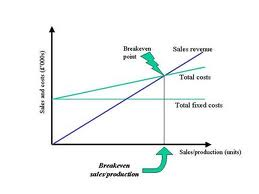

Break even is where you don't make a profit or a loss

{kind=link}

{kind=link}

19th November

Want to create your own Notes for free with GoConqr? Learn more.