4218012

Question 1

Question

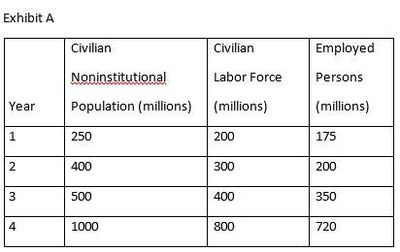

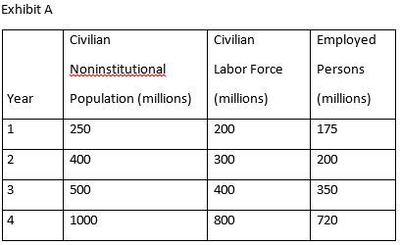

Refer to Exhibit A. The employment rate in year 4 is:

{kind=link}

Answer

-

12.5 %

-

7.2 %

-

72%

-

10%

-

90%

Question 2

Question

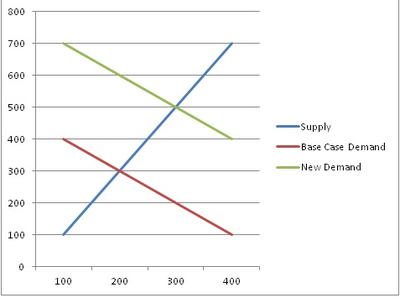

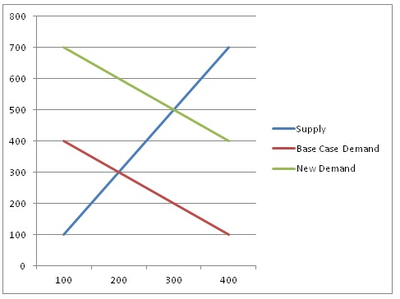

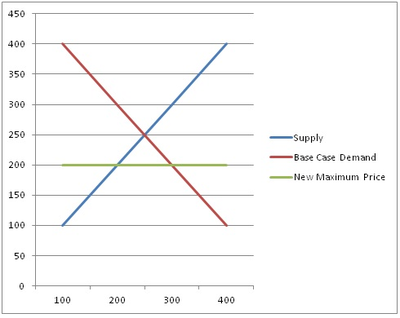

The graph below shows the market for llamas and how that market would change with a new law requiring every pizza delivery company that has had a delivery driver cause a traffic collision to switch to a llama only delivery system. The Y-Axis from 0 to 800 indicates price. The X-Axis from 0 to 400 indicates quantity.

What is the price per llama at the new equilibrium?

{kind=link}

Answer

-

$365,000

-

$0

-

$500

-

$300

Question 3

Question

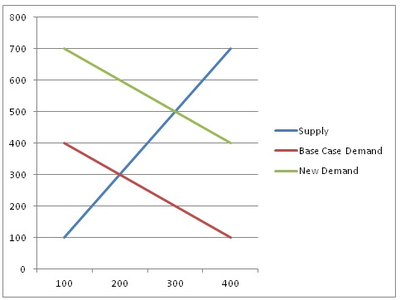

The graph below shows the market for llamas and how that market would change with a new law requiring every pizza delivery company that has had a delivery driver cause a traffic collision to switch to a llama only delivery system. The Y-Axis from 0 to 800 indicates price. The X-Axis from 0 to 400 indicates quantity.

What is the price per llama at the initial equilibrium?

{kind=link}

Answer

-

$200,000

-

$16.50

-

$500

-

$300

Question 4

Question

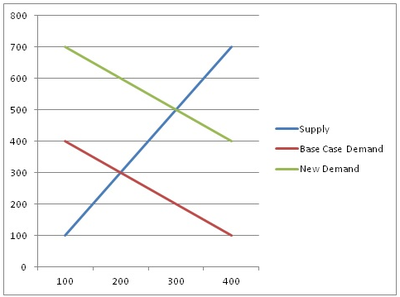

The graph below shows the market for llamas and how that market would change with a new law requiring every pizza delivery company that has had a delivery driver cause a traffic collision to switch to a llama only delivery system. The Y-Axis from 0 to 800 indicates price. The X-Axis from 0 to 400 indicates quantity

How would the price of llamas react under this policy if the supply of llamas was, unlike the graph, actually a constant due to breeding and health limitations?

{kind=link}

Answer

-

Llamas would escape and attack the citizens of Terrell.

-

The price of llamas would go up some but it would not reach the amount shown on the graph as the new equilibrium price.

-

The price of llamas would go down.

-

The price of llamas would go up and be higher than the amount shown on the graph as the new equilibrium price.

Question 5

Question

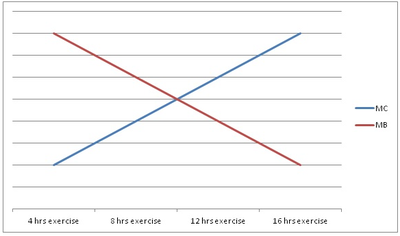

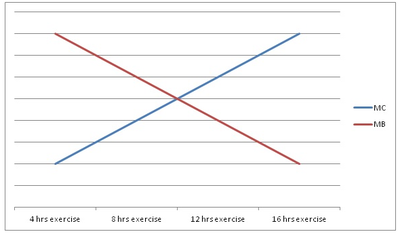

The graph below depicts the balance between the marginal benefits of exercise in terms of the number of times of exercise per week and the marginal costs of exercise in terms of the expenditure of time.

Opportunity Cost is related to this graph because:

{kind=link}

Answer

-

Economic actors have to give up something to enter the market and hire accountant to calculate these amounts

-

The transaction costs of owning a workout facility and being available to customers on a regular schedule are difficult for an entrepreneur to deliver on a consistent basis

-

The more you exercise, the more you are not doing something else. The something else you choose not to do can likely be of low value for the first 4 hours of weekly exercise but is likely of a higher value in the 13th to 16th hours of exercise. Thus, the MC curve is upward sloping reflecting opportunity costs.

-

The marginal benefit of all activities increase with increased consumption.

Question 6

Question

The graph below shows the market for llamas and how that market would change with a new law requiring every pizza delivery company that has had a delivery driver cause a traffic collision to switch to a llama only delivery system. The Y-Axis from 0 to 800 indicates price. The X-Axis from 0 to 400 indicates quantity. Is the movement from the Base Case Demand to the New Demand:

{kind=link}

Answer

-

A Change in the Quantity Demanded

-

A Change in Demand

-

Unfair Price Gouging by Suppliers

-

An opportunity to invest in an auto repair business

Question 7

Question

The following is a series of excerpts from an economics parable entitled “I, Pencil” by Leonard Read, recounted in video form on the nanocivics website by Milton Friedman.

I am a lead pencil—the ordinary wooden pencil familiar to all boys and girls and adults who can read and write. Writing is both my vocation and my avocation; that's all I do….

I am seemingly so simple. …. Yet, not a single person on the face of this earth knows how to make me. This sounds fantastic, doesn't it? Especially when it is realized that there are about one and one-half billion of my kind produced in the U.S.A. each year.

Pick me up and look me over. What do you see? Not much meets the eye—there's some wood, lacquer, the printed labeling, graphite lead, a bit of metal, and an eraser….

My family tree begins with what in fact is a tree, a cedar of straight grain that grows in Northern California and Oregon. Now contemplate all the saws and trucks and rope and the countless other gear used in harvesting and carting the cedar logs to the railroad siding. Think of all the persons and the numberless skills that went into their fabrication: the mining of ore, the making of steel and its refinement into saws, axes, motors; the growing of hemp and bringing it through all the stages to heavy and strong rope; the logging camps with their beds and mess halls, the cookery and the raising of all the foods. Why, untold thousands of persons had a hand in every cup of coffee the loggers drink!

The logs are shipped to a mill in San Leandro, California. Can you imagine the individuals who make flat cars and rails and railroad engines and who construct and install the communication systems incidental thereto? These legions are among my antecedents.

Consider the millwork in San Leandro. The cedar logs are cut into small, pencil-length slats less than one-fourth of an inch in thickness. These are kiln dried and then tinted for the same reason women put rouge on their faces. People prefer that I look pretty, not a pallid white. The slats are waxed and kiln dried again. How many skills went into the making of the tint and the kilns, into supplying the heat, the light and power, the belts, motors, and all the other things a mill requires? Sweepers in the mill among my ancestors? Yes, and included are the men who poured the concrete for the dam of a Pacific Gas & Electric Company hydroplant which supplies the mill's power! ….

My "lead" itself—it contains no lead at all—is complex. The graphite is mined in Ceylon. Consider these miners and those who make their many tools and the makers of the paper sacks in which the graphite is shipped and those who make the string that ties the sacks and those who put them aboard ships and those who make the ships. Even the lighthouse keepers along the way assisted in my birth—and the harbor pilots.

The graphite is mixed with clay from Mississippi in which ammonium hydroxide is used in the refining process. Then wetting agents are added such as sulfonated tallow—animal fats chemically reacted with sulfuric acid. After passing through numerous machines, the mixture finally appears as endless extrusions—as from a sausage grinder-cut to size, dried, and baked for several hours at 1,850 degrees Fahrenheit. To increase their strength and smoothness the leads are then treated with a hot mixture which includes candelilla wax from Mexico, paraffin wax, and hydrogenated natural fats.

My cedar receives six coats of lacquer. Do you know all the ingredients of lacquer? Who would think that the growers of castor beans and the refiners of castor oil are a part of it? They are. Why, even the processes by which the lacquer is made a beautiful yellow involve the skills of more persons than one can enumerate! ….

My bit of metal—the ferrule—is brass. Think of all the persons who mine zinc and copper and those who have the skills to make shiny sheet brass from these products of nature. Those black rings on my ferrule are black nickel. What is black nickel and how is it applied? The complete story of why the center of my ferrule has no black nickel on it would take pages to explain.

….no single person on the face of this earth knows how to make me…

The pencil story communicated the following important concepts related to price:

Answer

-

The market price is how much the corporate owner of the pencil making operation force people to pay.

-

The market price is the amount that the government sets because people need pencils and should not have to pay too much.

-

The market price of the pencil summarizes information about the supply and demand for the individual pieces of the pencil and rations the limited number pencils that are actually produced.

-

The market price of the pencil conceals the actual danger of using pencils as a substitute for chop sticks.

Question 8

Question

Gross Domestic Product (GDP) is the total market value of all

Answer

-

final goods and services produced annually within a country's borders

-

final and intermediate goods and services produced annually within a country's borders

-

intermediate goods and services produced annually within a country's borders

-

final goods and services produced every month within a country's borders

Question 9

Question

Read the passage from nanocivics.com below and then answer the following question:

The Invisible Hand is perhaps the most well-known economics turn of phrase. During a recession, it may seem not only invisible, but missing altogether. What does it really mean?

Here’s economist Peter Leeson, author of The Invisible Hook: The Hidden Economics of Pirates , on the question:

“In 1776 Scottish moral philosopher Adam Smith published a landmark treatise that launched the study of modern economics. Smith titled his book, An inquiry in the Nature of Cause of the Wealth of Nations. In it he described the most central idea to economics which he called the “invisible hand.” The invisible hand is the hidden force that guides economic cooperation. According to the Smith, people are self-interested; they’re interested in doing what’s best for them. However, often time, to do what’s best for them, people must also do what’s best for others.

The reason for this is straight forward. Most of us can only serve our self-interests by cooperating with others. We can achieve very few of our self-interested goals, from securing our next meal to acquiring our next pair of shoes, in isolation. Just think about how many skills you’d need to master and how much time you’re require if you had to produce your own milk or fashion your own coat, let alone manufacture our own car.

Because of this, Smith observed, in seeking to satisfy our own interests, we’re led, “as if by an invisible hand,” to serve others’ interests too. Serving others’ interests gets them to cooperate with us, serving our own. The milk producer, for example, must offer the best milk at the lowest price possible to serve his self interest, which is making money. Indirectly he serves his customers’ self-interest, which is acquiring cheap, high-quality milk. And on the other side of this, the milk producers’ customers, in their capacity as producers of whatever they sell, must offer the lowest price and highest quality to their customers, and so on. The result is a group of self-interest seekers, each narrowly focused on themselves but also unwittingly focused on assisting others.”

Here’s what Adam Smith, author of The Wealth of Nations , wrote:

“It is not from the benevolence of the butcher, the brewer or the baker, that we expect our dinner, but from their regard to their own interest. We address ourselves, not to their humanity but to their self-love, and never talk to them of our own necessities but of their advantages.”

That is, we pay the butcher and the baker a monetary price for their effort. We don’t tell them we are hungry and hope for the best; we give them the means to satisfy their own needs when we pay them. Thus, we ourselves had better find a way to satisfy someone else’s needs or else we won’t have the resources to pay for diner.

So that’s the invisible hand, the order in society generated by many people freely seeking their own, but only able to do so successfully by serving others.

by Mike Sims

According to Adam Smith’s work, which of the following describes the “invisible hand”?

Answer

-

Military elites secret control of raw materials

-

Wealthy elites in corporations controlling prices

-

Intellectual elites in government and the media controlling your beliefs and perceptions about the world

-

The uncoordinated activity of many who incidentally serve others in order to obtain the rationing device they desire for themselves

-

Sauron’s pursuit of the one ring that will rule them all

Question 10

Question

If the CPI is 100 in the base year and 140 in the current year, how much did prices rise between these two years?

Answer

-

40 percent

-

140 percent

-

1.40 percent

-

0.14 percent

Question 11

Question

In 2007, the U.S. GDP was approximately

Answer

-

$13.84 trillion

-

$5.15 trillion

-

$12.67 billion

-

$19.83 million

Question 12

Question

In the business cycle, what is the difference between the recovery phase and the expansion phase?

Answer

-

The expansion phase occurs in the rising portion of the business cycle, while the recovery phase occurs in the falling portion of the business cycle

-

The expansion phase occurs in the falling portion of the business cycle, while the recovery phase occurs in the rising portion of the business cycle.

-

The expansion phase is the period when Real GDP increases beyond the recovery phase

-

The expansion phase must always precede the recovery phase

Question 13

Question

Read the following selection and answer the question which follows:

There was a recent flap because three different members of the Obama administration, on three different Sunday television talk shows, gave three widely differing estimates of how many jobs the president has created.

The big question that seldom-- if ever-- gets asked in the mainstream media is whether these are a net increase in jobs. Since the only resources that the government has are the resources it takes from the private sector, using those resources to create jobs means reducing the resources available to create jobs in the private sector.

So long as most people do not look beyond superficial appearances, politicians can get away with playing Santa Claus on all sorts of issues, while leaving havoc in their wake-- such as growing unemployment, despite all the jobs being "created."

Whatever position people take on health care reform, there seems to be a bipartisan consensus-- usually a sign of mushy thinking-- that it is a good idea for the government to force insurance companies to insure people whom politicians want them to insure, and to insure them for things that politicians think should be insured.

… let's stop and think.

Why aren't insurance companies already insuring the people and the conditions that they are now going to be forced to cover? Because that means additional costs-- and because the insurance companies don't think their customers are willing to pay those particular costs for those particular coverages.

It costs politicians nothing to mandate more insurance coverage for more people. But that doesn't mean that the costs vanish into thin air. It simply means that both buyers and sellers of insurance are forced to pay costs that neither of them wants to pay. But, because soaring political rhetoric leaves out such grubby things as costs, it sounds like a great deal.

It is not just costs that are left out. It is consequences in general. With all the laments in the media about skyrocketing unemployment among young people, and especially minority young people, few media pundits even try to connect the dots to explain why unemployment hits some groups much harder than others.

Yet unusually high unemployment rates among young people is not something new or even something peculiar to the United States. Even before the current worldwide recession, unemployment rates were 20 percent or more among workers under 25 years of age in a number of Western European countries.

The young have less experience to offer and are therefore less in demand. Before politicians stepped in, that just meant that younger workers were paid less. But this is not a permanent situation because youth itself is not permanent, and pay rises with experience.

Enter politicians. By mandating a minimum wage that sounds reasonable for most workers, they put a price on inexperienced and unskilled labor that often exceeds what it is worth. Mandated pay rates, like mandated insurance coverage, impose on buyers and sellers alike things that they would not choose to do otherwise.

Workers of course prefer higher wage rates. But the very fact that the government has to impose those wage rates means that workers were unwilling to risk not having a job by refusing to work for less than the wage rate that has been mandated. Now that choice has been taken out of their hands, with the hidden cost in this case being higher unemployment rates.

By Thomas Sowell

This analysis encourages the reader to consider:

Answer

-

The marginal benefits and marginal costs faced by employers and employees.

-

Changes in economic behavior caused by changes in governmental policy.

-

Both of the above

-

None of the above

Question 14

Question

Economics is the study of:

Answer

-

Money

-

Scarcity

-

Abundance

-

Ecology

Question 15

Question

Suppose that 1982 is the base year for the Consumer Price Index (CPI) and in 2007 the CPI is 320. What does this "320" mean?

Answer

-

What cost $100 in 1982 will on average cost 320 times as much in 2007

-

What cost $100 in 1982 will on average cost $320 in 2007

-

What cost $100 in 1982 will on average cost 0.32 times as much in 2007 (that is, it will cost $32 in 2007)

-

What cost $100 in 1982 will on average cost $32 more in 2007

Question 16

Question

Economics categorizes resources into several categories, these are:

Answer

-

Money, Debt, Scarcity, and Abundance

-

Price, Quantity and Exchange

-

Land, Labor, Entrepreneurship and Capital

-

Investment, Labor, Natural Resources, and Finance

Question 17

Question

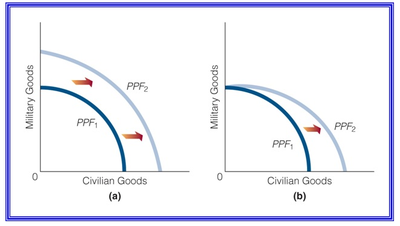

Something must be happening in the two Production Possibility Frontier graphs below that make them change in different ways. Which of the following best describes the difference between these two?

{kind=link}

Answer

-

In A, there has been tornado which destroyed both types of manufacturing capacity and caused a shift from PPF1 to PPF2. In B, there has been a tornado which destroyed only the civilian goods manufacturing capacity.

-

In A, there has been a technological breakthrough which helped all manufacturing equally and caused a shift from PPF2 to PPF1. In B, there has been technological breakthrough which helped only the military goods manufacturing capacity.

-

In A, there has been a productivity improvement for military goods and civilian goods causing the shift from PPF1 to PPF2. In B, there has been a productivity improvement for only civilian goods.

-

None of the above.

Question 18

Question

Water-proof poncho production increases under which of the following situations:

Answer

-

It stops raining and the forecast is for dry weather.

-

Pop-stars wearing water-proof ponchos to major events cause a general increase in the demand for ponchos; causing several existing clothing manufactures to get into the poncho production business.

-

Several traffic fatalities are blamed on the lack of visibility from hooded poncho wearing drivers; public acceptance for ponchos drops and surpluses of ponchos are sent to warehouses for storage.

-

New rules make poncho sales illegal in most international markets.

Question 19

Question

Refer to Exhibit A. How many people are not in the labor force in year 1?

{kind=link}

Answer

-

25 million

-

50 million

-

75 million

-

175 million

-

200 million

Question 20

Question

A recession is always part of a

Answer

-

Contraction

-

Recovery

-

Detraction

-

Party Mix Tape

Question 21

Question

When the opportunity cost of an activity is high, then:

Answer

-

The marginal costs go to zero.

-

The marginal benefits go to zero.

-

It must have high marginal benefits to be the subject of an economic exchange.

-

The transaction costs are low.

Question 22

Question

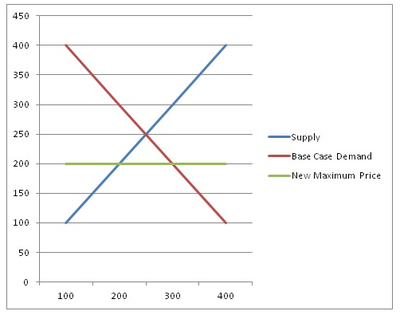

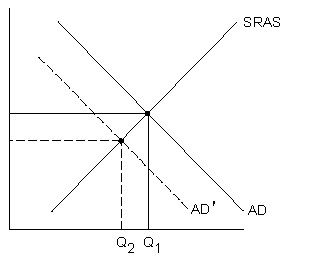

The graph below shows the market for llamas and how that market would change with a new law imposing a maximum price for llamas.

The new law will create:

{kind=link}

Answer

-

A price per llama that exceeds the base case

-

A shortage of llamas

-

A surplus of llamas

-

A new equilibrium that fully satisfies the supply and demand

Question 23

Question

The graph below depicts the balance between the marginal benefits of exercise in terms of the number of times of exercise per week and the marginal costs of exercise in terms of the expenditure of time.

The point of economic efficiency is:

{kind=link}

Answer

-

The end point of the Marginal Cost curve (MC).

-

Something that can be determined only through mathematical equations.

-

The starting point of the Marginal Benefit curve (MB).

-

The intersection of the MB curve and the MC curve.

Question 24

Question

The graph below shows the market for llamas and how that market would change with a new law imposing a maximum price for llamas.

Prior to the law, what was the market determined price for a llama?

{kind=link}

Answer

-

$200

-

$400

-

$250

-

$600

Question 25

Question

Consider the following equations:

Qd = 1500 - 32P

Qs = 1200 + 43P

Qd = Qs

Which statement is correct?

Answer

-

The equilibrium price is $16 and the equilibrium quantity is 5532.

-

The equilibrium price is $2 and the equilibrium quantity is 418.

-

The equilibrium price is $4 and the equilibrium quantity is 1372.

-

It is not possible to determine an answer from the information given.

Question 26

Question

According to the author, Keynes disagreed with previous economists regarding:

Answer

-

The importance of eco-friendly projects in long-term growth.

-

The importance of inflexible wages in preventing recovery.

-

The importance of America as a trading partner for Asian countries.

-

The importance of the exchange rate in the long-term.

Question 27

Question

Regarding the classical economics position with respect to (a) wages, (b) prices, and (c) interest rates, all three are considered by classical economics to be___________________, and to be determined by the interaction of supply and demand in their respective markets, leading to a position of equilibrium.

The correct missing phrase is:

Answer

-

intangible in long-term

-

incoherent under detailed scrutiny

-

flexible both up and down

-

inflexible either up or down

Question 28

Question

According to economists who believe in a self-regulating economy, what happens when the economy is in an inflationary gap?

Answer

-

Excess unemployment exists. This will cause wages to fall, and the SRAS curve will shift to the right, moving along the AD curve until the economy returns to its long-run equilibrium.

-

Unemployment is below its natural rate, creating wage inflation. This shifts the SRAS curve to the left, moving along the AD curve until the economy returns to its long-run equilibrium.

-

Hayek has to come and turn the knob that says, “reach equilibrium”.

-

None of the above.

Question 29

Question

What is the state of the labor market in a recessionary gap:

Answer

-

There is a labor market surplus.

-

There is a labor market shortage.

-

The labor market is in equilibrium.

-

The labor market is spastic.

Question 30

Question

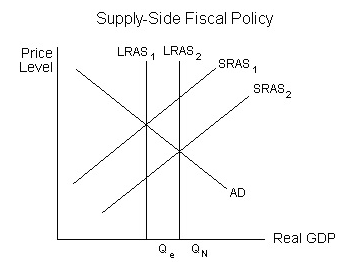

The graph below illustrates how government can use supply-side fiscal policy to get an economy out of a recessionary gap.

The following provides a correct explanation of the graph:

{kind=link}

Answer

-

The economy is in an inflationary gap at Qe. We implement a permanent income tax cut that moves SRAS to SRAS2 and LRAS to LRAS2, removing the gap at QN.

-

The economy is in a recessionary gap at Qe. We implement a permanent income tax increase that moves SRAS to SRAS2 and LRAS to LRAS2, removing the gap at QN.

-

The economy is in a inflationary gap at Qe. We implement a permanent income tax increase that moves SRAS to SRAS2 and LRAS to LRAS2, removing the gap at QN.

-

The economy is in a recessionary gap at Qe. We implement a permanent income tax cut that moves SRAS to SRAS2 and LRAS to LRAS2, removing the gap at QN.

Question 31

Question

The graph below shows Aggregate Demand and Short Run Aggregate Supply depicting a decrease in wealth.

What is the correct interpretation of the resulting new equilibrium:

{kind=link}

Answer

-

The price level will stay the same and Real GDP will fall .

-

The price level will fall and Real GDP will stay the same .

-

The price level will rise and Real GDP will rise .

-

The price level will drop and Real GDP will fall .

-

The price level will stabilize and Real GDP will oscillate .

Question 32

Question

Happy Birthday Keynes!

By Gouranga Das

Korean Times, June 10, 2009

June 5, 1883, is the birthday of John Maynard Keynes. Unlike other years, there is no other more opportune moment than this year, 125 years later, to wish him many happy returns.

Why? As has been said by Paul Samuelson: ``Science is a parasite: the greater the patient population the better the advance in physiology and pathology; and out of pathology arises therapy. The year 1932 was the trough of the great depression, and from its rotten soil was belatedly begot a new subject that today we call macroeconomics.''

And, Keynes was the founding father of modern macroeconomics as expounded in his famous treatise ``The General Theory of Employment, Interest, and Money'' (1936), following the outbreak of the Great Depression in late 1929, and spanning till 1932.

He said: ``I shall argue that the postulates of the classical theory are applicable to a special case only and not to the general case … Moreover, the characteristics of the special case assumed by the classical theory happen not to be those of the economic society in which we actually live, with the result that its teaching is misleading and disastrous if we attempt to apply it to the facts of experience.''

The classical economists predating Keynes put enormous faith on the self-correcting mechanism or forces that guaranteed full-employment and prevented cyclical fluctuations.

Emphasizing flexible prices ― wage and interest rates ― in stabilizing the economy precluded the need for government engagement for taming business cycles.

Without ascribing an important role for the government to intervene via expansionary or contractional fiscal and monetary policy, the burden of curing unemployment was shifted to wage stickiness or rigidity.

Thanks to Sir John Hicks, Nobel Laureate, and Alvin Hansen, Keynesian macroeconomics took its functional shape while couched in a ``working model,'' namely IS-LM developed in 1937.

The New Deal adopted by Roosevelt was based on non-existent economic theory and Keynes' theory gave birth to an intellectual framework to interpret events and offered a clear-headed argument for public policy.

The essential backbone was effective demand, multiplier effect of fiscal policy, liquidity preference and animal spirits (expectations not explained by rationality).

IS-LM rides again in a world of crisis caused by a ``financial debacle.'' According to The Economist (May 2, 2009), ``this year's downturn is much deeper than previous troughs'' in 1975, 1982, 1991 and 2001.

Global output is set to fall by 2.5 percent, unlike 0.4 percent on previous occasions. Unlike earlier cases, world trade, according to the International Monetary Fund (IMF) World Economic Outlook, is set to falter by 12 percent ― a setback to globalization.

As per the IMF forecast, G7 economies are heading for 0.1-percent growth, while for emerging economies like India and China it is 6 percent. Economies are nose-diving with the worst slump in decades since the 1930s.

Heavily export-dependent economies like Korea, Japan and China are facing the brunt of the slowdown or recessions hitting the United States and Europe. Manufacturing collapse is happening in these economies with the possibilities of a contagion of protracted recession.

With weakening demand, the need for products such as cars, semi-conductors, and consumer goods is evaporating. Companies such as Honda, Sony, Panasonic and Fuji have scaled back production as demand has dried up.

Korea's faltering exports and weak domestic demand are severe drags for the economy. China, Korea and Japan have entered into a joint agreement, including currency swap deals to stabilize the won's freefall against the greenback as investors retreated, cooperating to stimulate demand and ensure growth and stability.

Korea has also initiated government projects ― the Korean ``New Deal'' along with the ``Green New Deal'' (investing in 36 eco-friendly projects) ― to stimulate sluggish demand via job creation.

Japan has already called for a third round of spending worth $154 billion plus injecting 121 billion yen into regional banks to combat recession (The New York Times, March 17). It cannot be denied that despite the political rhetoric of no-tax and small government, most of the countries strike a balance between the public and private sectors. We do need ``Keynesian'' prognosis to cure the maladies.

With monetary policy being not so effective, aggressive fiscal policy maneuvering, by either cutting taxes or inducing demand, is a sensible way to avert the slump's evil. Resolute public policy has a prime-mover role in protecting the vulnerable and fragile economies, sufficient regulation, supervision of the financial systems and sustainable development. Although the mix, composition and scale of fiscal jolts are country-specific, handling catastrophe needs a fiscal ``magic'' wand to make it a shallow recession.

Now is the time to stop worrying about being Keynesian or anti-Keynesian, and rather work toward a synthesis of whatever is valuable in old and modern theories as necessary. In fact, George Akerlof and Robert Shiller have recently co-authored a book titled ``Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism.'' Their thesis states that factoring animal spirits such as irrational exuberance, confidence, corruption, fairness, money illusions and misplaced belief into economic theory would help avert the tragedy of crisis with the help of government.

Keynes' contribution has revolutionized the way intellectuals think about economic malaise and will do so in years to come. Keynes remarked, ``In the long run, we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is long past, the ocean will be flat again.''

With an appropriate stimulus package in the short-run, we won't be dead in the long run and a sound global economy could be reborn.

Gouranga Das is professor of economics at Hanyang University's Ansan campus in Gyeonggi Province.

The article refers to several countries for which the author advises adopting a Keynesian approach to improving the economic situation. In the author’s opinion, these countries should:

Answer

-

Adopt aggressive fiscal policy according to recent refinements to Keynesian theory.

-

Invade one another, causing damage consistent with the “broken window” theory.

-

Manipulate interest rates according to Friedman and Hayek’s theories.

-

The importance of the exchange rate in the long-term.

Question 33

Question

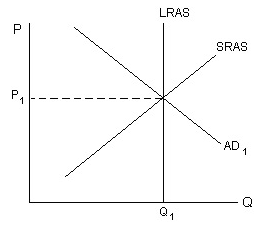

Candide believes that there is always sufficient (aggregate) demand in the economy to buy all the goods and services supplied at full employment, as shown in the graph below:

If true, the economy would always be at:

{kind=link}

Answer

-

Natural Real GDP, where P equals Q.

-

Natural Real GDP, where LRAS exceeds SRAS.

-

Natural Real GDP, where SRAS is a downward sloping line.

-

Natural Real GDP, where LRAS equals SRAS.

Question 34

Question

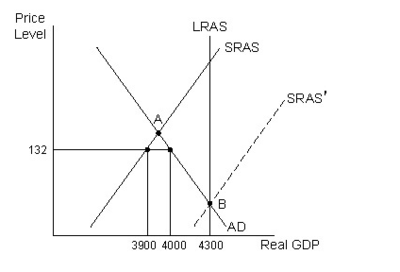

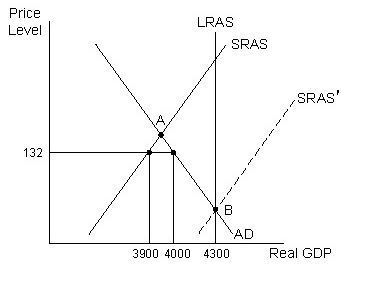

Suppose the economy is self-regulating, the price level is 132, the quantity demanded of Real GDP is $4 trillion (or $4,000 billion), and the quantity supplied of Real GDP in the short run is $3.9 trillion (or, $3,900 billion). Refer to the graph below.

Will the price level in the long-run equilibrium be greater than, less than, or equal to 132?

{kind=link}

Answer

-

Greater than 132

-

Equal to 132

-

Less than 132

-

Negative 132

Question 35

Question

Use the following table:

Taxable Income Taxes

$1,000-$5,000 10% of taxable income

$5,001-$10,000 $500 + 12% of everything over $5,000

$10,001-$15,000 $1,100 + 15% of everything over $10,000

$15,001 or more $1,850 +95% of everything over $15,000

If a day laborer’s income is $7,000, how much does he pay in taxes and how much does he keep?

Answer

-

$620 in taxes and $6,380 to keep

-

$730 in taxes and $6,270 to keep

-

$740 in taxes and $6,260 to keep

-

$850 in taxes and $6,150 to keep

Question 36

Question

What is the explanation for why investment falls as the interest rate rises?

Answer

-

The interest rate is the cost of borrowing funds. The higher the cost of borrowing funds is, the fewer funds firms will borrow and invest.

-

Bono’s Law: What you don’t have, you don’t need it now.

-

The cost of borrowing funds is balanced with changes in the stock market.

-

Equilibrium conditions such as this are not observed in the real world.

Question 37

Question

An increase in labor productivity would result in the following:

Answer

-

The price level will rise and Real GDP will rotate .

-

The price level will rise and Real GDP will stay the same .

-

The price level will stay the same and Real GDP will rise .

-

The price level will drop and Real GDP will fall .

-

The price level will fall and Real GDP will rise .

Question 38

Question

Happy Birthday, Milton Friedman!

By Gary S. Becker

Newsweek July 1, 2002

Milton Friedman's professional career has been marked by controversy over his many policy proposals. Yet as he approaches his 90th birthday in July, Friedman is increasingly recognized as the most influential economist in a 20th century that witnessed towering contributions from John Maynard Keynes, Paul A. Samuelson, and others.

Friedman is best known for "monetarism," a view that stability in the growth of the money supply is crucial to controlling inflation and recessions. Although the relation between the money supply and the economy has often been highly variable, no less an authority than Federal Reserve Chairman Alan Greenspan has indicated that Friedman's emphasis on a stable monetary framework was instrumental in guiding central banks in Europe and the U.S. toward low inflation during the past two decades.

Before Friedman, economic conventional wisdom held that inflation reduces unemployment because prices rise faster than labor costs. In the late 1960s, Friedman argued instead that there is no permanent reduction in unemployment from continuing inflation because wages eventually catch up to prices as expectations about inflation become more accurate. His analysis has been validated twice since then--by the high U.S. unemployment during the 1970s despite rapid inflation, and the low unemployment during the '90s even though inflation was negligible.

Some of Friedman's contributions to micro policy have been fully implemented, such as his persuasive advocacy of a voluntary army while serving on the Gates Commission set up to reconsider the draft after the Vietnam War. At a recent White House event to honor Friedman on his approaching birthday, I discussed a few of his policy proposals that have only been partially adopted and continue to generate controversy.

Two decades before Chile introduced its revolutionary private individual account retirement system, Friedman's classic 1962 book Capitalism and Freedom criticized the prevailing pay-as- you-go Social Security systems for restricting the ability of individuals to choose how much and in what form to save for retirement, and for mixing a welfare program for elderly poor with a compulsory program that applies to all the elderly. Had his advice been followed 20 years ago, there would be no impending Social Security financing crisis in the U.S. and other developed nations with aging populations.

In the same book, Friedman showed that without any change in the tax base, a flat income tax rate of 23% could bring in the same revenue as the system of rates that ranged in the 1960s from 20% to an incredible 91%. A few years later, he went further by demonstrating that the flat rate could be reduced to 16% without any diminution in tax revenue if all special deductions for mortgage interest, charitable contributions, and the like were eliminated. All nations have since brought down their top rates from frequently above 90% to 50% or less. So the world has moved about halfway toward his flat-tax system.

In the early 1950s, Friedman revived the case for allowing foreign exchange rates to be determined by supply and demand for different currencies. Flexible rates had fallen into intellectual disrepute because exchange rates were unstable during the 1930s, and after the post-World War II Bretton Woods Agreement introduced a worldwide system of supposedly fixed exchange rates.

Controversy over flexible exchange rates continues as American political leaders condemn Treasury Secretary Paul H. O'Neill for his refusal to seek a strong dollar. Meanwhile, exporters want him to promote a weak dollar that would make their goods cheaper to other nations. Secretary O'Neill is right in his commitment to let markets decide the international value of the dollar rather than government officials or business leaders with vested interests.

School vouchers is the micro program most closely identified with Friedman. In the 1950s, he first proposed that governments give tuition vouchers to parents with school-age children that they could use at private or public schools of their choice as long as these met education standards. He was confident that even poor parents would generally select a good education for their children if they had real choices.

Although voucher advocates have largely won the intellectual battle, vouchers have been effectively opposed by teachers' unions and by many suburban parents who fear vouchers would encourage poor children to attend schools in their communities. The U.S. Supreme Court will soon decide the legality of several voucher experiments.

Friedman has displayed enormous courage in sticking to his guns after his work was greeted with hostility and, frequently, nasty personal attacks. It must be gratifying to see how much the world has moved toward his positions. We all owe an enormous debt to this great economist as he completes his ninth decade.

Gary S. Becker, the 1992 Nobel laureate, teaches at the University of Chicago and is a Fellow of the Hoover Institution.

Whereas Keynes was concerned with government spending, the article emphasizes that thinkers like Milton Friedman (and Hayek) would more likely focus on:

Answer

-

Using school vouchers to balance international trade.

-

Using a flat tax to balance GDP with the CPI.

-

Stable interest rates and a predictable, transparent regulatory scheme to balance economic fluctuations.

-

Preparing young men and women to give their life in defense of their country as a way to reduce long-term labor supply and unemployment.

Question 39

Question

Use the following table:

Taxable Income Taxes

$1,000-$5,000 10% of taxable income

$5,001-$10,000 $500 + 12% of everything over $5,000

$10,001-$15,000 $1,100 + 15% of everything over $10,000

$15,001 or more $1,850 +95% of everything over $15,000

The table above an example of which kind of tax system:

Answer

-

The right-way to happiness system

-

A progressive tax system

-

A proportional or flat tax system

-

A fair tax, or a national consumption tax system

-

A regressive tax system

Question 40

Question

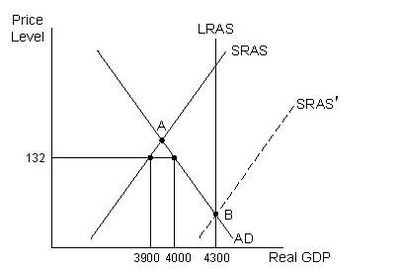

Suppose the economy is self-regulating, the price level is 132, the quantity demanded of Real GDP is $4 trillion (or $4,000 billion), and the quantity supplied of Real GDP in the short run is $3.9 trillion (or, $3,900 billion). Refer to the graph below.

What is the quantity supplied of Real GDP in the long run?

{kind=link}

Answer

-

$4.3 trillion or $4,300 billion

-

$4.0 trillion or $4,000 billion

-

$3.9 trillion or $3,900 billion

-

$132 billion

Question 41

Question

An increase in wealth would result in the following:

Answer

-

The price level will rise and Real GDP will fall .

-

The price level will rise and Real GDP will stay the same .

-

The price level will rise and Real GDP will rise .

-

The price level will drop and Real GDP will fall .

-

The price level will fall and Real GDP will fall .

Question 42

Question

An increase in wealth would:

Answer

-

Cause a movement along the aggregate demand line.

-

Cause a decrease in aggregate demand at every price.

-

Cause an increase in aggregate demand at every price.

-

Shift the short run aggregate supply line.

Question 43

Question

According to the author, the concept that Keynes was the better economist of the last 100 years:

Answer

-

Will forever be unquestioned.

-

Is accurate because Milton Friedman was wrong about exchange rates.

-

Will change when people find out about his rap career.

-

May be changing to recognize Milton Freidman instead.

Question 44

Question

Use the following table:

Taxable Income Taxes

$1,000-$5,000 10% of taxable income

$5,001-$10,000 $500 + 12% of everything over $5,000

$10,001-$15,000 $1,100 + 15% of everything over $10,000

$15,001 or more $1,850 +95% of everything over $15,000

If a doctor’s income is $115,000, how much does she pay in taxes and how much does she keep?

Answer

-

$1,500 in taxes and $113,500 to keep

-

$15,000 in taxes and $100,000 to keep

-

$5,850 in taxes and $109,150 to keep

-

$96,850 in taxes and $18,150 to keep

Question 45

Question

What factors will shift the AD curve in the simple Keynesian model?

Answer

-

Imports, Exports and Net Exports.

-

Consumption, Business Investment, and Government Purchases.

-

Land, Labor and Capital

-

Taxes, Regulation, and International Exchange Rates

Question 46

Question

The Minimum Wage and Job Loss from 2006 through 2010

By Staff at the Political Calculations Blog

March 9, 2011

In 2006, the last full year in which the U.S. federal minimum wage was a constant value throughout the whole year, at least before 2010, approximately 6,595,383 individuals in the United States earned $7.25 per hour1 or less.

For 2010, the first full year in which the U.S. federal minimum wage was a constant value through the year since 2006, the U.S. Bureau of Labor Statistics estimates that an average of just 4,361,000 individuals in the United States earned the same equivalent of the current prevailing federal minimum wage of $7.25 or less throughout the year.

In terms of jobs lost, that means that 2,234,383 of the jobs lost in the U.S. economy since 2006 have been jobs that were directly impacted by the series of minimum wage increases that were mandated by the federal government in 2007, 2008 and 2009.

Interestingly, the average number of employed members of the civilian labor force in 2006 was 144,427,000. In 2010, the average number of employed members of the civilian labor force in the U.S. was 5,363,000 less, standing at 139,064,000.

So, in percentage terms of the change in total employment level from 2006 to 2010, jobs affected by the federal minimum wage hikes of 2007, 2008 and 2009 account for 41.8% of the total reduction in jobs seen since 2006.

What would Hayek or Freidman say about this data:

Answer

-

This is an example of how Keynes’ sticky wages are not a free market dynamic, but a government regulatory dynamic.

-

Instead of using fiscal stimulus to fix a problem caused by government regulation, simply deregulate the labor market to remove government induced sticky wages.

-

The good feelings caused by passing a minimum wage increase are out-weighed by the real-world negative impact on the people who can no longer find employment.

-

All of the above.

Question 47

Question

If wage rates are not flexible, can the economy be self-regulating?

Answer

-

No, to achieve a “favorable” balance of trade a country must bring gold and silver into the country and that will maintain domestic employment.

-

No, according to both the agricultural system of the physiocrats and the laissez-faire of the nineteenth and early twentieth centuries,

-

No, flexible wages are an essential assumption of the self-regulating economy. Without flexible wages, the SRAS curve would not shift in response to an inflationary gap or a recessionary gap. Without this flexibility, the economy could not move back to its long-run equilibrium, and the economy would not be self-regulating.

-

Yes, because I gravitate to answering yes and this is the only answer with the word yes in it.

Question 48

Question

Suppose the economy is self-regulating, the price level is 132, the quantity demanded of Real GDP is $4 trillion (or $4,000 billion), and the quantity supplied of Real GDP in the short run is $3.9 trillion (or, $3,900 billion). Refer to the graph below.

In the starting condition (SRAS), is the economy in short-run equilibrium?

{kind=link}

Answer

-

Yes, SRAS and LRAS are equal

-

Yes, SRAS is less than LRAS

-

No, AD is greater than SRAS

-

No, AD is less than SRAS

Question 49

Question

What is the explanation for why saving rises as the interest rate rises?

Answer

-

The interest rate is the cost of borrowing funds. The higher the cost of borrowing funds is, the more funds firms will borrow and invest.

-

The higher the interest rate, the higher the reward for saving (or the higher the opportunity cost of consuming), and therefore, the fewer funds consumed and the more funds saved.

-

The interest rate is the cost of borrowing funds. The lower the cost of borrowing funds is, the more funds firms will borrow and invest.

-

The higher the interest rate, the higher the reward for saving (or the higher the opportunity cost of consuming), and therefore, the more funds consumed and the more funds saved.

Question 50

Question

What does it mean to say the economy is in a recessionary gap?

Answer

-

In a recessionary gap, Real GDP < Natural Real GDP.

-

In a recessionary gap, Real GDP > Natural Real GDP.

-

In a recessionary gap, Real GDP = Natural Real GDP.

-

In a recessionary gap, Real GDP - CPI < Zero

Question 51

Question

If the Federal Reserve were to conduct an open market purchase, how would money supply change?

Answer

-

Money supply will increase

-

Money supply will decrease

-

Money supply will stay the same

-

It cannot be determined from the information provided

Question 52

Question

How will action by the Federal Reserve to lower the discount rate impact the money supply?

Answer

-

Money supply will increase

-

Money supply will decrease

-

Money supply will stay the same

-

It cannot be determined from the information provided

Question 53

Question

U.S. Inflation Targeting: Pro and Con

FRBSF Economic Letter, 98-18; May 29, 1998

In recent years, monetary economists and central bankers have expressed growing interest in inflation targeting as a framework for implementing monetary policy. Explicit inflation targeting has been adopted by a number of central banks around the world, including those in Australia, Canada, Finland, Israel, New Zealand, Spain, Sweden, and the U.K. In the United States, there has been little public debate over inflation targeting, although some bills have been introduced in Congress to mandate the use of explicit targets for inflation.

Issues and questions surrounding inflation targeting formed a major focus of a recent conference on Central Bank Inflation Targeting jointly sponsored by the Federal Reserve Bank of San Francisco and the Center for Economic Policy Research at Stanford University (Rudebusch and Walsh 1998). In this Economic Letter, we set out some of the arguments for and against adopting inflation targeting in the United States discussed at the conference. (For further discussion, see Bernanke and Mishkin 1997, Bernanke, et al., forthcoming, and Keleher 1997.)

What would inflation targeting mean in the U.S.?

There has been some ambiguity about the precise definition of an inflation targeting policy regime, in part because certain institutional arrangements have differed from one inflation targeting country to another--most notably with regard to how the inflation target is set and how deviations from the target are tolerated. For our discussion, we define inflation targeting to be a framework for policy decisions in which the central bank makes an explicit commitment to conduct policy to meet a publicly announced numerical inflation target within a particular time frame. For example, at the start of 1993, Sweden's central bank announced an inflation target for the consumer price index of between 1 and 3 percent by 1995. Similarly, if the Federal Reserve wanted to adopt inflation targeting, it would publicly commit to achieving a particular numerical goal for inflation (a target point or range) within a set time span of, say, a couple of years. Also, as part of an ongoing policy framework for targeting inflation, the Fed's semiannual Humphrey-Hawkins report, which currently provides a near-term (one-year) outlook for inflation, could be augmented to include a discussion of whether the medium-term (two- or three-year) inflation forecast is consistent with the announced medium-term inflation target. Inflation targeting would not impose a rigid simple rule for the Fed; instead, policy could employ some discretion to take into account special shocks and situations. However, the organizing principle and operational indicator for monetary policy would be focused on inflation and (in light of lags in the effects of policy) inflation forecasts.

Given some earlier ambiguity, it is important to be clear about how we interpret the ultimate goals of inflation targeting monetary policy. In particular, an inflation targeting central bank need not care only about inflation. Indeed, most inflation targeting central banks continue to recognize multiple goals for monetary policy with no single primary one. (In New Zealand--an exception--the start of inflation targeting coincided with a legislative mandate that the central bank's "primary function" was price stability, while in Canada--as is more typical--such legislation was never passed.) Accordingly, an operational policy framework of inflation targeting would still be consistent with the Fed's current legislated objectives of low inflation and full employment. An inflation targeting regime can accommodate a goal of output stabilization by having wide inflation target bands, long inflation target horizons, and explicit exemptions for supply shocks. Thus, the adoption of an inflation targeting regime does not necessarily require that price stability or low inflation be the preeminent goal of monetary policy. As with monetary targeting, inflation targeting is an operational framework for monetary policy, not a statement of ultimate policy goals. (For further discussion, see Rudebusch and Svensson, 1998.)

Arguments pro

By focusing attention on a goal the Fed can achieve, by making monetary policy more transparent and increasing public understanding of the Fed's strategy and tactics, by creating institutions that foster good policy, and by improving accountability, the adoption of inflation targeting would represent a desirable change in the U.S. monetary policy.

1. The announcement of explicit inflation targets for the Fed would provide a clear monetary policy framework that would focus attention on what the Fed actually can achieve. Bad monetary policy often has resulted from demands that central banks attempt to achieve the unachievable. Most notably, few macroeconomists believe that monetary policy can be used to lower the average rate of unemployment permanently, but central banks often are pressured to achieve just that through expansionary policy; such policy instead only results in higher average inflation without leading to a systematically lower average rate of unemployment. In contrast, implementing explicit inflation targets would help to insulate the Fed from such political pressure.

2. Transparent inflation targets in the U.S. would help anchor inflation expectations in the economy. When making real and financial investment decisions and planning for the future, businesses and individuals must form expectations about future inflation. Inflation targets would provide a clear path for the medium-term inflation outlook, reducing the size of inflation "surprises" and their associated costs. Inflation targets also likely would boost the Fed's credibility about maintaining low inflation in the long run, in part, because they mitigate the political pressure for expansionary policy. Since long-term interest rates fluctuate with movements in inflation expectations, targeting a low rate of inflation would lead to more stable and lower long-term rates of interest. Together, the reduced uncertainty about future medium-term and long-term inflation would have beneficial effects for financial markets, for price and wage setting, and for real investment.

3. The establishment of inflation targets in the U.S. would help institutionalize good monetary policy. Recent U.S. monetary policy has been generally considered excellent, but earlier in the postwar period, monetary policy clearly failed by allowing inflation to ratchet up significantly several times. To some extent, the quality of policy over time has reflected the skills and attitudes of the people involved in the policy process. Monetary policy is an area in which it is especially important to implement institutional structures that will help to avoid bad policies. Inflation targets can provide this institutional structure and help ensure that monetary policy is not dependent on always having the good luck to appoint the best people.

4. In the current system, there is some ambiguity about how and why the Fed operates. For example, although monetary aggregates play a very modest role in the policy process,they are the only variables that the Fed is required to set target ranges for and report about to Congress. As noted above, inflation targets would focus discussion on what the Fed actually could achieve. Furthermore, an inflation target provides a clear yardstick by which to measure monetary policy. Given forecasts of future inflation, it is easy to compare them to the announced inflation target and hence judge the appropriate tightness or looseness of current monetary policy. Also, on a retrospective basis, an explicit target allows Fed performance to be easily monitored. Thus, Congress and the public will be better able to assess the Fed's performance and hold it accountable for maintaining low inflation.

Arguments con

Inflation targeting, even without imposing a rigid rule, would unduly reduce the flexibility of the Fed to respond to new economic developments in an uncertain world. Furthermore, publicly committing solely to an inflation target would not enhance overall accountability or transparency given the multiple objectives of monetary policy.

1. The purpose of inflation targeting is to focus the attention of monetary policy on inflation. However, concentrating on numerical inflation objectives (even with caveats or escape clauses) also reduces the flexibility of monetary policy, especially with respect to other policy goals. That is, inflation targets place some constraints on the discretionary actions of central banks. Such constraints can be quite appropriate in countries where monetary policy has performed poorly, exhibiting sustained unproductive inflationary tendencies; however, this is not the case in the United States. U.S. monetary policy has operated quite well for almost two decades, so limiting the flexibility and discretion of the Fed to respond to new economic developments would be ill-advised. Why change a system that is working? Certainly, adept policymakers are one reason for the good performance of recent monetary policy, but there is also a strong institutional structure--stronger than existed at the start of the 1970s--that is already in place at the Fed that fosters good monetary policy.

2. Monetary policy requires the careful balancing of competing goals--financial stability, low inflation, and full employment--in an uncertain world. There is uncertainty about the contemporaneous state of the economy, the impact policy actions will have on future economic activity and inflation, and the evolving priority to be given to different policy objectives. However, because monetary policy actions affect inflation with a lag, inflation targeting means, in practice, that the Fed would need to rely heavily on forecasts of future inflation. Given the uncertainties the Fed faces, an inflexible and undue reliance on inflation forecasts can create policy problems. For example, most forecasts in the mid-1990s of inflation in the late 1990s over-estimated the inflation we are currently experiencing. If the Fed had been inflation targeting in the mid-1990s, it might well have raised the funds rate based on its inflation forecasts. Yet with today's low inflation and robust economy, it is difficult to argue that the Fed was too expansionary and that the more contractionary policy implied by inflation targeting would have produced a better outcome. As in this instance, it seems unlikely that a mechanical dependence on inflation forecasts to achieve inflation targets will improve policy.

3. Proponents of inflation targeting argue that it promotes accountability. However, as is generally agreed, low inflation is only one of the objectives of monetary policy. While monetary policy may not affect average real growth or unemployment over time, it does have an important role to play in helping to stabilize the economy. Even if average inflation is the one thing the Fed can control in the long run, it does not follow that the Fed should be held accountable only for its inflation record. Inflation targeting actually could reduce the Fed's overall accountability by allowing it to avoid responsibility for damping short-run fluctuations in real economic activity and unemployment. Making the Fed publicly accountable for only one policy goal may make it harder for Congress and others to monitor the Fed's contribution to good overall macroeconomic policy.

4. Similarly, with regard to the transparency and public understanding of policy, inflation targeting highlights the inflation objective of central banks but tends to obscure the other goals of policy. Just as uncertainty about future inflation impedes good economic decision making, so does uncertainty about the future level of output and employment. Inflation targeting sweeps the latter concerns under the rug (often by adjusting the amount of time that deviations are allowed from the inflation target). Given the multiple legitimate goals of policy, the single public focus of inflation targeting does not enhance overall transparency.

Glenn D. Rudebusch, Research Officer and Carl E. Walsh, Professor of Economics, UC Santa Cruz

Under inflation targeting, the organizing principle and operational indicator for monetary policy would be focused on:

Answer

-

Unemployment and labor force participation.

-

Inflation and inflation forecasts.

-

Gold prices and the dollar exchange rate.

-

Managing the debt of the Federal Government and Social Security.

Question 54

Question

U.S. Inflation Targeting: Pro and Con

FRBSF Economic Letter, 98-18; May 29, 1998

In recent years, monetary economists and central bankers have expressed growing interest in inflation targeting as a framework for implementing monetary policy. Explicit inflation targeting has been adopted by a number of central banks around the world, including those in Australia, Canada, Finland, Israel, New Zealand, Spain, Sweden, and the U.K. In the United States, there has been little public debate over inflation targeting, although some bills have been introduced in Congress to mandate the use of explicit targets for inflation.

Issues and questions surrounding inflation targeting formed a major focus of a recent conference on Central Bank Inflation Targeting jointly sponsored by the Federal Reserve Bank of San Francisco and the Center for Economic Policy Research at Stanford University (Rudebusch and Walsh 1998). In this Economic Letter, we set out some of the arguments for and against adopting inflation targeting in the United States discussed at the conference. (For further discussion, see Bernanke and Mishkin 1997, Bernanke, et al., forthcoming, and Keleher 1997.)

What would inflation targeting mean in the U.S.?

There has been some ambiguity about the precise definition of an inflation targeting policy regime, in part because certain institutional arrangements have differed from one inflation targeting country to another--most notably with regard to how the inflation target is set and how deviations from the target are tolerated. For our discussion, we define inflation targeting to be a framework for policy decisions in which the central bank makes an explicit commitment to conduct policy to meet a publicly announced numerical inflation target within a particular time frame. For example, at the start of 1993, Sweden's central bank announced an inflation target for the consumer price index of between 1 and 3 percent by 1995. Similarly, if the Federal Reserve wanted to adopt inflation targeting, it would publicly commit to achieving a particular numerical goal for inflation (a target point or range) within a set time span of, say, a couple of years. Also, as part of an ongoing policy framework for targeting inflation, the Fed's semiannual Humphrey-Hawkins report, which currently provides a near-term (one-year) outlook for inflation, could be augmented to include a discussion of whether the medium-term (two- or three-year) inflation forecast is consistent with the announced medium-term inflation target. Inflation targeting would not impose a rigid simple rule for the Fed; instead, policy could employ some discretion to take into account special shocks and situations. However, the organizing principle and operational indicator for monetary policy would be focused on inflation and (in light of lags in the effects of policy) inflation forecasts.

Given some earlier ambiguity, it is important to be clear about how we interpret the ultimate goals of inflation targeting monetary policy. In particular, an inflation targeting central bank need not care only about inflation. Indeed, most inflation targeting central banks continue to recognize multiple goals for monetary policy with no single primary one. (In New Zealand--an exception--the start of inflation targeting coincided with a legislative mandate that the central bank's "primary function" was price stability, while in Canada--as is more typical--such legislation was never passed.) Accordingly, an operational policy framework of inflation targeting would still be consistent with the Fed's current legislated objectives of low inflation and full employment. An inflation targeting regime can accommodate a goal of output stabilization by having wide inflation target bands, long inflation target horizons, and explicit exemptions for supply shocks. Thus, the adoption of an inflation targeting regime does not necessarily require that price stability or low inflation be the preeminent goal of monetary policy. As with monetary targeting, inflation targeting is an operational framework for monetary policy, not a statement of ultimate policy goals. (For further discussion, see Rudebusch and Svensson, 1998.)

Arguments pro

By focusing attention on a goal the Fed can achieve, by making monetary policy more transparent and increasing public understanding of the Fed's strategy and tactics, by creating institutions that foster good policy, and by improving accountability, the adoption of inflation targeting would represent a desirable change in the U.S. monetary policy.

1. The announcement of explicit inflation targets for the Fed would provide a clear monetary policy framework that would focus attention on what the Fed actually can achieve. Bad monetary policy often has resulted from demands that central banks attempt to achieve the unachievable. Most notably, few macroeconomists believe that monetary policy can be used to lower the average rate of unemployment permanently, but central banks often are pressured to achieve just that through expansionary policy; such policy instead only results in higher average inflation without leading to a systematically lower average rate of unemployment. In contrast, implementing explicit inflation targets would help to insulate the Fed from such political pressure.

2. Transparent inflation targets in the U.S. would help anchor inflation expectations in the economy. When making real and financial investment decisions and planning for the future, businesses and individuals must form expectations about future inflation. Inflation targets would provide a clear path for the medium-term inflation outlook, reducing the size of inflation "surprises" and their associated costs. Inflation targets also likely would boost the Fed's credibility about maintaining low inflation in the long run, in part, because they mitigate the political pressure for expansionary policy. Since long-term interest rates fluctuate with movements in inflation expectations, targeting a low rate of inflation would lead to more stable and lower long-term rates of interest. Together, the reduced uncertainty about future medium-term and long-term inflation would have beneficial effects for financial markets, for price and wage setting, and for real investment.

3. The establishment of inflation targets in the U.S. would help institutionalize good monetary policy. Recent U.S. monetary policy has been generally considered excellent, but earlier in the postwar period, monetary policy clearly failed by allowing inflation to ratchet up significantly several times. To some extent, the quality of policy over time has reflected the skills and attitudes of the people involved in the policy process. Monetary policy is an area in which it is especially important to implement institutional structures that will help to avoid bad policies. Inflation targets can provide this institutional structure and help ensure that monetary policy is not dependent on always having the good luck to appoint the best people.

4. In the current system, there is some ambiguity about how and why the Fed operates. For example, although monetary aggregates play a very modest role in the policy process,they are the only variables that the Fed is required to set target ranges for and report about to Congress. As noted above, inflation targets would focus discussion on what the Fed actually could achieve. Furthermore, an inflation target provides a clear yardstick by which to measure monetary policy. Given forecasts of future inflation, it is easy to compare them to the announced inflation target and hence judge the appropriate tightness or looseness of current monetary policy. Also, on a retrospective basis, an explicit target allows Fed performance to be easily monitored. Thus, Congress and the public will be better able to assess the Fed's performance and hold it accountable for maintaining low inflation.

Arguments con

Inflation targeting, even without imposing a rigid rule, would unduly reduce the flexibility of the Fed to respond to new economic developments in an uncertain world. Furthermore, publicly committing solely to an inflation target would not enhance overall accountability or transparency given the multiple objectives of monetary policy.

1. The purpose of inflation targeting is to focus the attention of monetary policy on inflation. However, concentrating on numerical inflation objectives (even with caveats or escape clauses) also reduces the flexibility of monetary policy, especially with respect to other policy goals. That is, inflation targets place some constraints on the discretionary actions of central banks. Such constraints can be quite appropriate in countries where monetary policy has performed poorly, exhibiting sustained unproductive inflationary tendencies; however, this is not the case in the United States. U.S. monetary policy has operated quite well for almost two decades, so limiting the flexibility and discretion of the Fed to respond to new economic developments would be ill-advised. Why change a system that is working? Certainly, adept policymakers are one reason for the good performance of recent monetary policy, but there is also a strong institutional structure--stronger than existed at the start of the 1970s--that is already in place at the Fed that fosters good monetary policy.

2. Monetary policy requires the careful balancing of competing goals--financial stability, low inflation, and full employment--in an uncertain world. There is uncertainty about the contemporaneous state of the economy, the impact policy actions will have on future economic activity and inflation, and the evolving priority to be given to different policy objectives. However, because monetary policy actions affect inflation with a lag, inflation targeting means, in practice, that the Fed would need to rely heavily on forecasts of future inflation. Given the uncertainties the Fed faces, an inflexible and undue reliance on inflation forecasts can create policy problems. For example, most forecasts in the mid-1990s of inflation in the late 1990s over-estimated the inflation we are currently experiencing. If the Fed had been inflation targeting in the mid-1990s, it might well have raised the funds rate based on its inflation forecasts. Yet with today's low inflation and robust economy, it is difficult to argue that the Fed was too expansionary and that the more contractionary policy implied by inflation targeting would have produced a better outcome. As in this instance, it seems unlikely that a mechanical dependence on inflation forecasts to achieve inflation targets will improve policy.

3. Proponents of inflation targeting argue that it promotes accountability. However, as is generally agreed, low inflation is only one of the objectives of monetary policy. While monetary policy may not affect average real growth or unemployment over time, it does have an important role to play in helping to stabilize the economy. Even if average inflation is the one thing the Fed can control in the long run, it does not follow that the Fed should be held accountable only for its inflation record. Inflation targeting actually could reduce the Fed's overall accountability by allowing it to avoid responsibility for damping short-run fluctuations in real economic activity and unemployment. Making the Fed publicly accountable for only one policy goal may make it harder for Congress and others to monitor the Fed's contribution to good overall macroeconomic policy.

4. Similarly, with regard to the transparency and public understanding of policy, inflation targeting highlights the inflation objective of central banks but tends to obscure the other goals of policy. Just as uncertainty about future inflation impedes good economic decision making, so does uncertainty about the future level of output and employment. Inflation targeting sweeps the latter concerns under the rug (often by adjusting the amount of time that deviations are allowed from the inflation target). Given the multiple legitimate goals of policy, the single public focus of inflation targeting does not enhance overall transparency.

Glenn D. Rudebusch, Research Officer and Carl E. Walsh, Professor of Economics, UC Santa Cruz

The article discusses inflation targeting. What entity would implement this policy?

Answer

-

The Federal Reserve

-

The U.S. Department of the Treasury

-

Individual Federal Reserve Districts such as the Federal Reserve Bank of San Francisco

-

The World Trade Organization

Question 55

Question

Not Enough Money

From the Apr. 4, 2011, issue of National Review.

‘To economists reading this essay in 2010, perhaps the most remarkable single fact to note about monetary policy at the end of the interwar period” — the author, Columbia University economist Charles Calomiris, is of course also talking about the end of the Great Depression — “is that its architects were, for the most part, quite pleased with themselves. Far from learning about the errors of their ways during the interwar period, Fed officials congratulated themselves on having adhered to appropriate principles, and to the extent that they were self-critical, it was because they thought that they had been too expansionary.”

Almost all economists today agree that monetary policy during the Depression, especially its early stages, was disastrously tight, indeed that this contractionary policy is the principal reason the Depression became Great. But perhaps we should not judge the central bankers of America in the 1930s too harshly. For one thing, as Calomiris notes, smart economists are still arguing about the precise nature of the Fed’s policy mistakes. He himself presents evidence against the received view that the Federal Reserve precipitated the “recession within a recession” of 1937 by raising banks’ reserve requirements and thus discouraging lending.

More important — and more disturbing — is that it is not at all clear that we have learned from the mistakes of the 1930s. Those central bankers believed that money was easy because interest rates were low and the monetary base (the supply of money under the Fed’s control) had expanded. They worried that further easing would reduce confidence in the dollar. British economist R. G. Hawtrey, writing in the late 1930s, described the climate of opinion in his country at the start of the decade: “Fantastic fears of inflation were expressed. That was to cry ‘Fire! Fire!’ in Noah’s Flood.” The economy was actually deflating, not inflating. Under the influence of the “real-bills doctrine,” some central bankers believed that the money supply should respond only to traders’ need for credit. Anything else would only fuel speculative excess.

Today’s inflation hawks employ the same reasoning that those firefighters did. And they are not wholly wrong. Easier money can lead to a destabilizing run on the currency. Inflation can be associated with low real interest rates and an expanded monetary base. But not always: Not in the 1930s, and almost certainly not today, either. The late Milton Friedman, perhaps the most famous inflation hawk of his generation, spotted the fallacy in his analysis of 1990s Japan:

Low interest rates can also be a symptom of an excessively tight monetary policy that has choked off opportunities for growth. A looser policy, by increasing expectations of future economic growth, could actually raise real interest rates.

To see why changes in the monetary base are also an unreliable guide to whether money is loose or tight, I’m afraid it’s necessary to look at an equation. Friedman and others familiarized us with the equation of exchange: MV=PY. What that means is that the money supply (M) times the speed with which money changes hands (V, for velocity) must equal the price level (P) times the size of the real economy (Y). If velocity holds constant and the money supply goes up, either prices must go up or the economy must expand or both.