7877094

Description

Flashcards by Sophie Knight, updated more than 1 year ago

|

|

Created by Sophie Knight

almost 8 years ago

|

|

| Question | Answer |

| How is Marginal Revenue Calculated? | Change in total revenue Change in Quantity |

| What will the total, marginal and average revenue curves look like when price is constant? | Total revenue is an upward sloping curve Average and marginal revenue curves are identical and horizontal at the given price level. |

| What is the difference between short run, long run and very long run production? | In the short run, at least one factor of production is fixed In the long run, all factors of production are variable In the very long run, the state of technology could change |

| What is the law of diminishing returns? | If increasing quantities of a variable input are combined with a fixed input, eventually the marginal product and then the average product of that variable input will decline |

| What are constant returns to scale? | If an equal percentage increase in inputs to production leads to the same percentage increase in output. |

| What is total product? | Quantity of output produced by a given number of inputs over a period of time. |

| What is a fixed (indirect or overhead) cost? | A cost that does not vary directly without output. |

| What is the condition for revenue maximisation? | When marginal revenue is zero |

| Draw the Total Product curve | . |

| Draw the AP and MP curves | . |

| What is the economic cost of depreciation? | Purchase Price - second hand value |

| What is a variable cost? | A cost that varies directly with output, as production increases, so does the variable costs. Also known as prime or direct cost |

| Give an example of a semi-variable cost that a firm may face | Labour as permanent staff will be fixed and part-time/ temporary workers will be variable. |

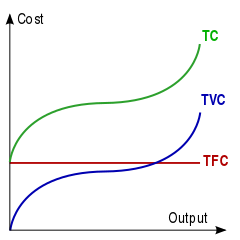

| Draw the TC, TFC and TVC curves | . |

| How could the position of the TFC curve be described? | Horizontal line at the value of the difference between the TC and TVC curves. |

| What are the 2 qualities of the Marginal Cost curve? | 1) Falls and then rises again as diminishing returns sets in (tick shaped) 2) Cuts the AVC and ATC curves at their lowest points |

| Draw the AFC, ATC, AVC and MC curves on the same set of axis | |

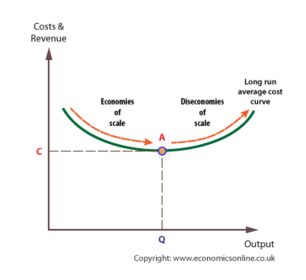

| How are economies and diseconomies shown on a diagram? | |

| What is the minimum efficient scale of production? | The point at which productive efficiency occurs (lowest minimum average cost) |

| Name 4 sources of economies of scale | 1) Financial 2) Technical 3) Purchasing and marketing 4) Managerial (specialisation) |

| What are the 2 main causes of diseconomies of scale? | 1) Poor management 2) Geographical issues in transporting goods |

| Give 4 reasons for a shift in the LRAC curve | 1) External economies of scale 2) Taxation 3) Technology 4) External diseconomies of scale |

| What are 3 ways of avoiding diseconomies of scale? | 1) Developments in human resource management 2) Performance-related pay schemes 3) Outsourcing of manufacturing and distribution |

| What is supernormal profit? | Profit above the normal profit line (break even point) Attracts new firms into the industry |

| How could maximum profit level be shown with TR and TC curves? | Where the gap between the two is the largest, which is where the gradients of the curve are equal |

| What are the 5 functions of profit? | 1) To pay out dividends to shareholders to stop them selling 2) Prevent takeovers due to lack of profit 3) A measure of business success 4) Source of investment 5) Market-signal |

| What are 3 Microeconomic effects of falling profits? | 1) No incentive to join markets, reducing competition 2) Pressure to reduce costs resulting in falling output and/or quantity 3) Reduced economies of scale |

| What are 4 Macroeconomic effects of falling profits? | 1) Less tax being paid, fall in government revenue 2) Interest rates likely to rise 3) Unemployment rises 4) Growth slows |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.