2113901

Description

Flashcards by claire.harrison, updated more than 1 year ago

|

|

Created by claire.harrison

almost 10 years ago

|

|

| Question | Answer |

| Relevance | Financial Information is said to be relevant if : - It has the ability to influence the economic decisions of the users - It is provided in time to influence those decisions |

| Reliability | Valuations (such as depreciation or inventory) must be; - Free from bias - Free from material errors - With a degree of caution (prudence) |

| Comparability | Information is much more useful if it is comparable over time and also with similar information about other businesses. |

| Ease of Understanding | Users should be able to understand with a reasonable knowledge of accounting and have a willingness to study the information diligently. |

| Materiality | Materiality defines the threshold or cut-off point after which financial information becomes relevant to the decision making needs of the users. |

| Statement of Profit or Loss (SPL) | Summary of Activity in the year Income Expenses |

| Statement of Financial Position (SPF) | Snapshot of the business on final day of accounting period Assets Liabilities Capital |

| SPL - Example | |

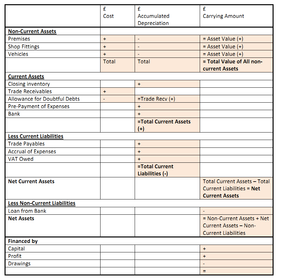

| SFP - Example | |

| SFP Non-Current Assets | Premises Shop Fittings Vehicles |

| SFP Current Assets | Closing Inventory Trade Receivables (minus Allowance DD) Pre-Payment of Expenses Bank |

| SFP Current Liabilities | Trade Payables Accrual of Expenses VAT Owed |

| SFP Non-Current Liabilities | Loan from Bank Mortgage |

| SFP Financed By | Capital + Profit - Drawings (Should match Net Assets) |

| SFP Net Assets | Non-Current Assets + Net Current Assets - Non-Currnet Liabilities = NET ASSETS |

| SPL Gross Profit | Sales Revenue - Sales Returns =SALES +Opening Inventory +Purchases -Purchases Returns -Closing Inventory =COST OF SALES SALES - COST OF SALES = GROSS PROFIT |

| SPL Additional Income | Discount Received Rent Received Profit on Disposal Allowance for DD Adjustment (CR) |

| SPL Expenses | General Expenses Interest Paid Wages Discount Allowed Irrecoverable Debts Depreciation Allowance DD Adjustment (DR) Loss on Disposal |

| SPL Overview | Gross Profit + Additional Income – Expenses = Net Profit / Loss |

| Accruals | SFP Current Liability |

| Allowance For Doubt Debts | SFP (Removed from SLCA - Trade Receivables) |

| Accumulated Depreciation | SFP Removed from Assets in the Accumulated Depreciation Column |

| Pre-Payments | SFP Current Asset |

| Allowance for Doubtful Debts Adjustments | SPL Expenses |

| Opening Inventory | SPL |

| SLCA Sales Ledger Control Account | SFP Trade Receivables - Remove Allowance for Doubtful Debts before posting to the SFP |

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.